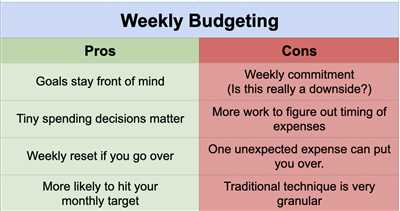

Creating a budget is an essential part of managing your finances. It allows you to have a clear view of your income and expenses, and helps you make smart financial decisions. While making a monthly budget is a common practice, breaking it down into a weekly budget can make it easier to track your spending and save money.

When it comes to making a weekly budget, it’s important to start by reviewing your monthly income and expenses. Take a close look at all the bills you need to pay each month, such as your mortgage or rent, utilities, and insurance. Then, divide these costs by four to get an idea of how much you’ll need to set aside each week.

Next, consider your variable expenses, such as groceries, eating out, and shopping. These expenses can vary from week to week, so it’s important to estimate an average amount. Look at your past spending habits and take into account any special events or occasions that may affect your spending.

- How to Make a Weekly Budget

- 1. Understand Your Income

- 2. Identify Your Expenses

- 3. Prioritize Your Expenses

- 4. Create Spending Categories

- 5. Set Financial Goals

- 6. Track Your Spending

- 7. Review and Adjust

- Collect Your Expenses

- Then find all your committed expenses

- Where do you put monthly income in your weekly budget

- Where to put your monthly income in your budget

- How to make budgeting easier

- The Bottom Line

- 1. Collect all the information

- 2. Review your income

- 3. Understand your expenses

- 4. Set a budget for each category

- 5. Put your budget into action

- Video:

- How I Budget my Paychecks 💸 paycheck breakdown, bi-weekly budget with me & more

How to Make a Weekly Budget

Creating a weekly budget is an important part of managing your finances. It allows you to track your income and expenses on a weekly basis, helping you stay on top of your financial goals. Here are some steps to help you create a weekly budget:

1. Understand Your Income

The first step in creating a weekly budget is to understand your income. Calculate how much money you earn per week, taking into account any additional sources of income.

2. Identify Your Expenses

Next, identify your expenses for the week. This includes fixed expenses such as rent or mortgage payments, utility bills, and insurance premiums. It also includes variable expenses such as groceries, eating out, and entertainment.

3. Prioritize Your Expenses

Once you have identified your expenses, prioritize them based on importance. Make sure to allocate enough funds for essential expenses such as food, housing, and transportation. This will help you determine how much you can allocate towards discretionary expenses.

4. Create Spending Categories

Divide your expenses into different categories, such as transportation, groceries, entertainment, and debt repayment. This will make it easier for you to track and manage your spending.

5. Set Financial Goals

Set financial goals for the week, such as saving a certain amount of money or paying off a specific debt. Having clear goals will help you stay motivated and committed to your budget.

6. Track Your Spending

Keep track of your expenses throughout the week. Use a budgeting app or simply jot down your expenses in a notebook. This will give you a clear picture of where your money is going and help you identify areas where you can cut back.

7. Review and Adjust

At the end of each week, review your budget and evaluate your spending habits. Identify any areas where you went over budget and find ways to improve. Adjust your budget for the following week accordingly.

By following these steps, you can make a weekly budget that aligns with your financial goals and helps you stay on track with your spending. Remember, budgeting is a skill that takes time and practice to master, so be patient with yourself as you navigate your financial journey.

Collect Your Expenses

When it comes to making a weekly budget, it is important to collect and understand all of your expenses. By knowing where your money is going, you can make smart financial decisions and ensure that you are on track to reach your financial goals.

Start by reviewing your monthly bills and payments. This includes your mortgage or rent, utilities, insurance, and any other recurring expenses. Make a list of each expense and their respective amounts.

Next, take a look at your weekly expenses. This includes things like groceries, transportation costs, dining out, and any other discretionary spending. It may be helpful to keep track of these expenses over a week or two to get an accurate understanding of your spending habits.

On an annual basis, review your other financial obligations such as school loans, credit card bills, and any other outstanding debts. Understanding the terms of these loans will help you identify areas where you can save money, such as through consolidation or refinancing options.

While collecting your expenses, it is important to also review your credit reports and scores. This will help you identify any potential issues, such as identity theft or errors on your reports, that may be affecting your financial health. Websites like Experian offer free credit reports and scores, making it easier than ever to stay on top of your credit.

Once you have collected all of your expenses and reviewed your financial information, you can start to create a budget. This budget should align with your income and financial goals, ensuring that you are committed to saving while also meeting your financial obligations.

Remember to include a contingency plan in your budget. Life is unpredictable, and having an emergency fund in place can provide peace of mind and financial security. Put aside a small amount each week to build up your savings over time.

In conclusion, collecting your expenses is an important part of budgeting. By understanding where your money is going, you can make informed decisions about your spending and saving habits. This will put you on the right track to achieving your financial goals and improving your overall financial situation.

Then find all your committed expenses

Once you have a clear understanding of your income and financial goals, it’s time to identify and list all your committed expenses. These are the bills and payments that you have to make each week, regardless of other factors. By categorizing and tracking them, you can better plan your budget and ensure that you have enough money to cover these expenses.

Start by collecting all your financial documents, including bank statements, credit card bills, loan agreements, and mortgage documents. Review them carefully to identify all the fixed expenses you have. This may include rent or mortgage payments, utility bills, insurance premiums, and loan repayments.

It’s important to include all your committed expenses, even if they seem small or infrequent. Take into account things like annual subscription fees, medical bills, and school fees. These may not occur every week, but when they do, it’s essential to account for them in your budget.

Identify companies or services that automatically deduct payments from your bank account or credit card. These could be monthly subscriptions, such as streaming services or gym memberships. Include these in your list of committed expenses as well.

While you may not have control over the timing or terms of these expenses, understanding them will help you make better financial decisions. By knowing the full extent of your committed expenses, you can evaluate if there are ways to improve your budget or negotiate better terms with certain companies.

Many people find it helpful to organize their committed expenses using a budgeting planner or spreadsheet. This can make it easier to see the big picture and identify areas where you may be overspending or have room to save. Plus, having a written list of your expenses can serve as a constant reminder to stay on track with your budget goals.

Remember, the goal of identifying your committed expenses is to have a complete picture of your financial obligations. It’s an essential step in creating a realistic and effective weekly budget. By being aware of all your expenses, you can make informed decisions about how to allocate your income and prioritize your spending.

Where do you put monthly income in your weekly budget

When creating a weekly budget, it’s important to consider where you will allocate your monthly income. This will help you properly plan and manage your finances to ensure that you have enough money for all of your expenses throughout the month.

One common method is to divide your monthly income into four equal parts, one for each week of the month. This way, you can allocate a specific amount for each week’s expenses, such as groceries, transportation, entertainment, and other miscellaneous costs.

You can start by listing all of your fixed monthly expenses, such as rent or mortgage payments, utility bills, and any other recurring bills. These should be included in your budget as they are essential payments that need to be made on a regular basis.

Next, consider any variable expenses that you expect to occur each week. This can include things like eating out, shopping, or any other non-essential spending. You can allocate a specific amount for these expenses or choose to limit them to a certain budget to manage your overall spending.

It’s also important to consider any annual or quarterly expenses that may occur during a specific week. These can include things like car insurance payments or annual memberships. By factoring in these expenses, you can ensure that you set aside money each week to cover these costs when they arise.

If you have any debt or loans, it’s important to prioritize these payments in your budget as well. You can allocate a certain portion of your monthly income to pay off these debts, helping you improve your credit scores and financial health over time.

It’s a good idea to review your budget on a weekly basis to make sure you’re staying on track. You can make adjustments as needed, such as shifting money from one week to another or cutting back on certain expenses if necessary.

Where to put your monthly income in your budget

One effective way to manage your weekly budget is by using a budgeting tool or app. There are many options available, both free and paid, that can help you track your income and expenses. These tools often provide visual representations of your budget, making it easier to see where your money is being allocated each week.

You can also create a simple budgeting spreadsheet or use a pen and paper to jot down your income and expenses. This can be a more manual approach, but it can still be effective for those who prefer a more hands-on experience.

How to make budgeting easier

While budgeting may seem daunting at first, there are several ways to make the process easier and more manageable. Here are a few tips:

- Automate your savings by setting up automatic transfers from your checking account to a savings account.

- Use cash for discretionary spending to help you stick to your budget and avoid overspending.

- Prioritize your expenses and eliminate any non-essential spending that may be draining your budget.

- Consider using the envelope system, where you allocate a specific amount of cash to different categories of expenses.

- Take advantage of free financial resources and educational materials provided by reputable companies and financial institutions.

Remember, budgeting is an important part of managing your finances and achieving your financial goals. By taking the time to plan and allocate your monthly income in your weekly budget, you can improve your financial health and make smarter financial decisions.

The Bottom Line

Creating a weekly budget can be a smart financial move, as it allows you to have a clear understanding of your income, expenses, and savings goals. By taking the time to review your expenses and set a budget for each week, you can stay on top of your finances and make sure you are putting your money towards the things that are most important to you. Here are some steps to help you make a weekly budget:

1. Collect all the information

Before you can start budgeting for the week, gather all your financial information in one place. This includes bills, credit card statements, loan payments, and any other expenses you may have. It’s important to have a full understanding of where your money is going each month.

2. Review your income

Take a look at your monthly income and determine how much you make each week. This will give you a clear picture of how much money you have available to budget with.

3. Understand your expenses

Make a list of all your expenses, both fixed and variable. Fixed expenses include things like rent or mortgage payments, insurance premiums, and monthly bills. Variable expenses include items such as groceries, eating out, and shopping. By categorizing your expenses, you can identify areas where you can save money or cut back.

4. Set a budget for each category

Once you have a clear understanding of your expenses, set a budget for each category. This will ensure that you allocate your money in a way that aligns with your financial goals. Be realistic with your budget and make sure it’s achievable.

5. Put your budget into action

Now that you have your budget set, commit to sticking to it for the week. This may require some adjustments in your spending habits, but it will ultimately help you save money and achieve your financial goals.

While budgeting can seem overwhelming at first, there are tools and resources available to make it easier. For example, the Consumer Financial Protection Bureau (CFPB) offers a budgeting worksheet and a budgeting planner to help you stay on track. Additionally, there are online budgeting tools and apps that can help you track your expenses and see where your money is going.

Understanding the bottom line of your budget is important. By taking the time to review your financial situation each week, you can make informed decisions about your money and ensure that you are on track to meet your long-term financial goals.

Remember, budgeting is a continuous process and may require adjustments along the way. Be flexible and open to making changes as needed. With commitment and perseverance, you can achieve financial success and peace of mind.